Long Matthews International (MATW)

Get the stock price up, or get fired

“A man always has two reasons for doing anything: a good reason and the real reason.”

J.P. Morgan

Hello OpTrackers,

Today we are back with a write up on a long opportunity: Matthews International (MATW).

Company Overview

Matthews International is a very old conglomerate, going all the way back to 1850. And in the fashion of old school conglomerates, it has multiple segments with absolutely nothing to do with each other. And I mean nothing.

The company’s key segments are as follows:

Memorialization: This segment essentially manufactures caskets. There are some other cemetery and funeral home products in here, but think of it as a casket manufacturer.

Industrial Technologies: This segment has two main business lines. The first is the production of calendaring equipment that is used in the production of lithium-ion batteries used in EVs. The second is warehouse automation related products.

SGK Brands: This segment is a marketing business. And its particular strength lies in the design and development of packaging.

The company has a pitch that these segments are somehow related. And if you squint hard enough warehouse automation is vaguely tangential to packaging design, I guess, but honestly no one is buying it so don’t think too hard about it.

Lastly, like most write-ups my style, the specifics of what the business do aren’t super important, so we don’t need to spend a ton of time on the specifics.

Now, turning to the financials. Here is a quick summary of the segment disclosures over the last couple of years:

Overall, this has been an unexciting but steady-eddy business and (until recently) was very levered (~$850mm of net debt).

With the basics of the business, let’s get into the story and why this boring business looks like an interesting opportunity.

Situation Background

In short, Matthews International has been a really poor investment for a really long time. Below is a chart that compares MATW’s share price to the S&P 500, the Nasdaq, and the Russell 2000. Now, given the companies size and industry, totally fair to say that the S&P 500 and Nasdaq are unfair comps, but I think the Russell is totally fair and really I just want to make the point that - pick any index you want - MATW compares unfavorably.

A negative TSR over 10 years is just pretty abysmal, especially for this type of business.

Unsurprisingly, when you have a business performing this bad in modern capital markets, an activist shows up. The activist in question here is Barington and you can find their website for the Matthews campaign here.

Barington actually “won” the campaign in a pyrrhic way, with ISS and Glass Lewis recommending their proxy card.

However, Matthews had some nice activism defense advice from the guys at Sidley and management’s card won the ultimate vote. It came at a cost, though. In order to win the vote of the Headless Horsemen of Passive Investing (Blackrock, Vanguard, State Street and Dimensional own 35% of the MATW’s stock) the company had to de-stagger the board and replace a couple of directors.

GAMCO also published a letter in support of the company’s nominees, but specifically called out that it could go the other way in 2026 if the board does not improve the situation by the next annual meeting.

The de-staggering of the board is important and we will come back to it, because it leaves the company more vulnerable going forward.

SGK Divestiture

THE PLOT THICKENS. Because in the middle of the proxy contest, MATW agreed to merge their SGK segment into a competitor, SGS. As part of the transaction, MATW will get $250mm of cash upfront, $50mm of preferred equity in the new entity, it will retain $50mm of receivables, and it gets 40% of the common equity in the pro forma company. The company has said they expect minimal tax leakage from the transaction:

That is effectively $300mm of cash upfront and a stake in a business that I don’t really know what it’s worth, but the transaction values the pro forma entity at $900mm of TEV at 9x $100mm of EBITDA. Even if you assume half the TEV is debt, 40% of $450mm of equity value is another $180mm of value to MATW plus the $50mm of preferred equity is $230mm of value “on the come”. But let’s haircut it arbitrarily and call it another $150mm of value.

On top of this, MATW retained a couple of businesses from within the SGK segment that it subsequently sold for another $50mm.

Okay, so summing this all up, MATW is getting a total of $350mm of cash upfront and another potential $150mm+ of value from its residual stake in the pro forma SGK entity.

Pro Forma Matthews

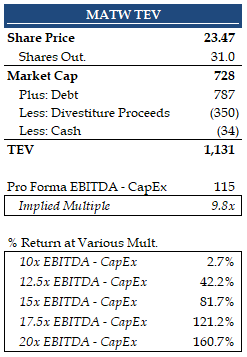

Pro Forma for the divestiture, I think the math on MATW looks like roughly the following:

The Pro Forma EBITDA - CapEx is just taking 2024’s figures, subtracting the EBITDA - CapEx contribution from SGK and then reducing corporate costs to $45mm, which management as indicated is a fair run-rate going forward.

The range of multiples I am using for the valuation is based on the chart below, which is the TEV / NTM EBIT multiples from Capital IQ. CapEx and D&A are pretty close for MATW, so I think it’s a reasonable proxy.

If you ignore the crazy COVID period, MATW has basically always traded within the 10-20x EBIT range and so that’s the range of multiples I am using. Note, CapIQ isn’t doing any adjustments to the TEV for the divestitures, so the most recent data can be ignored - we’re really just looking at the long-term range as bookends.

And those multiples get us 0 - 160% upside. And that’s not giving the company any credit for what could be $200mm+ of value for their remaining stake in the SGS + SGK combo. That’s not too bad!

Where Does This Leave Us?

So, MATW is a historically very poorly performing company from a stock price perspective, though at least recently the operating results have not been disastrous.

An activist is involved in the company, actually won the proxy advisors over, but the company pulled off a stick-save by making some concessions that make them even more vulnerable to the activist the next go around.

In my opinion, management now recognizes they have a metaphorical gun to their head. If the stock is still trading where it is the next time election season rolls around, the board will be out of a job and they know it. Hence the proactive actions around SGK.

This means, come hell or high water, management the board either need to 1) sell the pieces and/or the entire company in the next year or 2) get the stock price up in the next year. To that end, I expect if the company does not decide to sell itself in its entirety, it will begin to aggressively repurchase shares after paying down some debt as a way to support the stock.

And if none of that happens, I expect the activist will run another campaign in 2026, win, and then the business will be sold. A year is a long time under the current US political regime and anything can happen, but I like our odds.

Questions for Dear Reader?

Am I missing something obvious here? Let me know in the comments or over on Twitter.

One obvious question I don’t have the answer to is: why does this opportunity exist? I don’t have a neat and tidy explanation for why the market has a less sanguine view of the stock than I do even after the notable SGK monetization. What do you all think?

Until next time, OpTrackers! Happy hunting!

Disclaimer: As always please remember nothing written in this blog should be considered investment advice. You should assume that even though we tried our best that this post is riddled with errors and do your own research/consult a licensed financial advisor before investing any of your own money into any financial security.